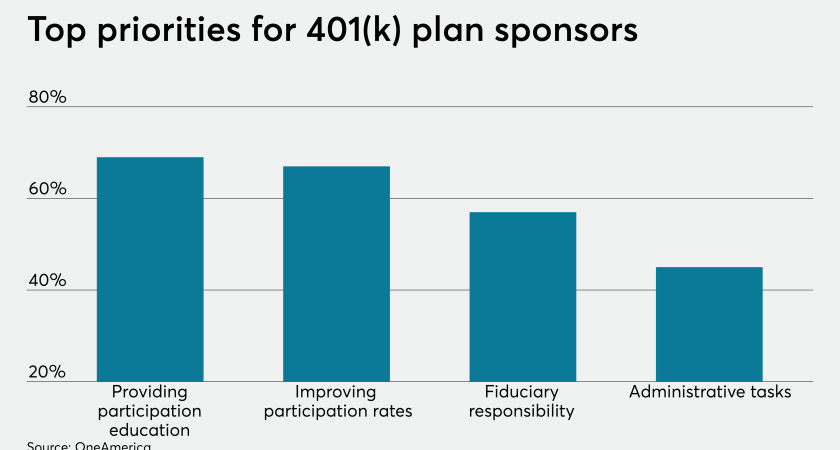

The big mistakes employers make when setting up 401(k) plans

American workers are in bad retirement shape. The gap between what employees need to save for retirement and what they are actually saving is widening, according to a report from the World Economic Forum.

Throughout my career as a CFP and plan adviser, I’ve seen firsthand how easy it is to miss big on making the most of workplace retirement plans. Employers assume that by making a 401(k) plan available to their team, they’re setting them on a track for financial stability. But in a world where people are living longer than ever — thanks to advances in healthcare and technology — and pensions are no longer the norm, just having a DC plan is not enough.

It’s in the best interest of employers to ensure their employees have a solid 401(k) and retirement plan. Companies who demonstrate an active interest in the financial wellness of their employees will be rewarded with more productive, less stressed workers, studies show.

With all of that being said, employers are still making some common mistakes when setting up their retirement plans. By addressing these issues employers can help ensure that their employees are making the most of their 401(k)s.

Not auto-enrolling employees in your 401(k) plan

When people are dealing with the pressures of settling into a new job — and the multitude of emails and forms that typically go along with it — tasks like setting up a 401(k) account can easily fall by the wayside. One of the best ways to ensure your employees actually start saving for retirement is to auto-enroll them. Some employees, particularly those from younger generations, may not fully understand the value of a 401(k) or what it does, or simply don’t want to take the time to figure out how to set up an account.

Auto-enrollment takes the work out of it for the employee and ensures they’re saving for retirement from the start. For employers concerned about taking action on behalf of employees — not only do employees have the option to change their contribution rate, but you’re setting an initial impression that this is an important choice to consider.

Choosing a low auto-enrollment rate

Now that you’ve gotten comfortable with the idea of opting people into the plan, you have to consider the contribution rate you’ll start employees off with. Not wanting to surprise them with a big cut out of their paycheck, you decide to go with a rate like 3% of pay. Sounds good, right? Wrong.

Ideally, employees should aim to contribute at least 6% to 8%, if not 10% to get on track to self-fund their retirement. With a low initial contribution rate, you may think you’re helping employees ease into savings, but instead you’re telling them that this is a good and sufficient rate for them to save.

Employers should opt-in with savings rates more in line with those needed to meet retirement goals. Worried about employee reactions with higher auto-enrollment rates? A study by John Beshears and Shlomo Benartzi showed no greater opt-out rate, and incrementally higher average savings rates, when participants were showed default rates between 6% and 11% of their incomes.

The issue of low default rates can be compounded if your company offers a match that requires a rate higher than the plan’s auto-enroll rate. By not meeting the full match, your employees are missing out on free savings. One third of workers don’t contribute enough to their 401(k) to receive their company’s match, according to Vanguard, which is just throwing away free money.

Relying on education materials and sessions to inspire action

We hear from employers that they want more education and more information for their employees to make the most of their 401(k) plans. They’re not wrong — people need to be empowered when making financial decisions. But how the information is delivered can make all the difference.

Picture this: you set up an education session for employees with a representative from your 401(k) plan service provider; they come armed with colorful literature about what retirement means to you, how to calculate what to save and how to build a diversified portfolio. A number of employees shuffle in, though many can’t be bothered. Those that do come in listen, slightly bored, during the presentation and walk out with brochures and paperwork.

How many of those employees do you think will return with the paperwork completed to get enrolled in the plan? How many do you think feel empowered, understanding how their savings rate today builds the retirement picture they want?

Information and decision-making should go hand-in-hand with the tools available to implement those decisions, at the right point in time. When working with a provider, look for a mix of experiences. Some people want to work directly with a representative to set up their account and understand how to get on the right track; others want to interact with online tools that help them easily land at a personalized savings rate based on their inputs, showing their potential retirement income based on what they can do today.

When people have the right tools at their fingertips, they’re more likely to engage in their own financial planning, take steps to implement their plan from the start, and feel empowered and on-track for retirement.

With just a few small changes to plan designs and financial tools, employers can help ensure their workers are making the most of their 401(k)s and are on track toward achieving the retirement they deserve.