Student loan benefits poised to take off

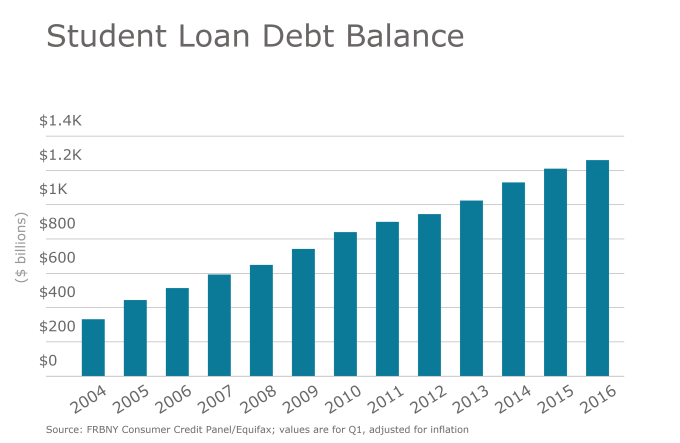

Saddled with about $30,000 of student loan debt and lower wages than their parents were making at their age, millennials and Gen Z are forgoing traditional saving strategies to tackle existing debt.

The changing workforce demographic has created a new protocol for HR departments to follow, which includes updating the benefits package to resonate with younger employees.

The average debt-to-salary for 20 to 30-year-olds is 60% to 70% or higher — and this debt is stifling, according to Scott Thompson, the CEO of student loan reimbursement platform company Tuition.io. “As we explore the data here and we give that to employers, they’re beginning to understand the real true benefit” of debt relief programs, he says.

Although only 4% of employers currently offer student loan repayment benefits, according to the Society of Human Resource Management, that number is increasing.

Citing a 2016 Willis Towers Watson survey, Thompson estimates the percentage of employers that will offer this benefit will increase to 25% to 30% over the next year.

Companies such as Aetna, brokerage firm Crystal & Company and Estée Lauder Companies are now offering about $10,000 in lifetime contributions to employees’ student loans. The monthly stipend is applied to an employee’s principal on the loan, which helps the employee pay off the loan faster and save on interest.

Companies look to student loan repayment providers like Tuition.io and Gradifi — the latter is used by Big Four firm PwC — to administer the benefit.

The benefit is not tax-treated, however, which makes it a difficult offering for the majority of companies to squeeze into their ever-growing benefits package.

That might change, however. U.S. Rep. Rodney Davis (R-Illinois) introduced the Employer Participation in Student Loan Assistance Act in 2017, but Congress has yet to act.

“Congress understands the size of the problem,” says Rob Reiskytl, a partner at Aon. “I think the difficulty is if you take action to enact legislation, it represents a tax loss.”

Existing legislation allows companies to offer up to $5,250 in tuition reimbursement, but employees are often looking to pay off existing student debt, not take on more.

Employers are capitalizing on this by slowly distributing a lump sum over five to eight years, which increases retention rates if employees want to take full advantage of the benefit.

Companies that can’t offer student loan reimbursement payments often opt for other benefits, such as consolidation programs and refinancing arrangements, according to Willis Towers Watson’s 2018 Emerging Trends: Voluntary Benefits and Services Survey.

The consulting firm anticipates 34% of employers will offer student loan consolidation programs by 2021, up from 8% in 2018, and 35% of employers will offer student loan refinancing arrangements by 2021, up from 10% in 2018.

“They might want to tackle the issue of student loan debt, but they want to tackle it as a broad perspective,” Reiskytl says. “Sometimes as employers, we fall into the trap of solving a problem without understanding the context in which the problem presents itself. The issue of student loan debt lives in a bigger financial ecosystem in an employee’s life.”